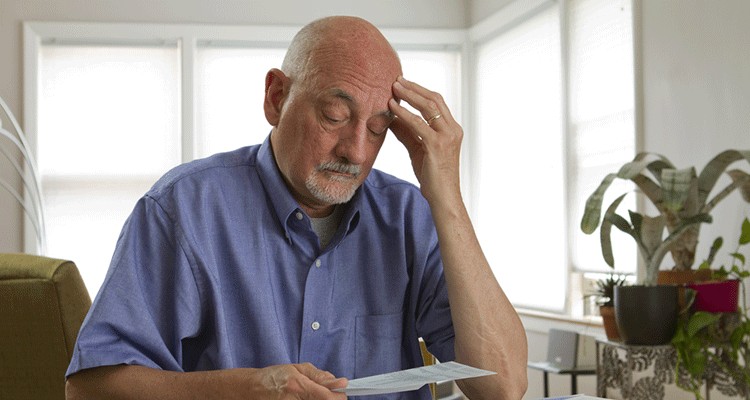

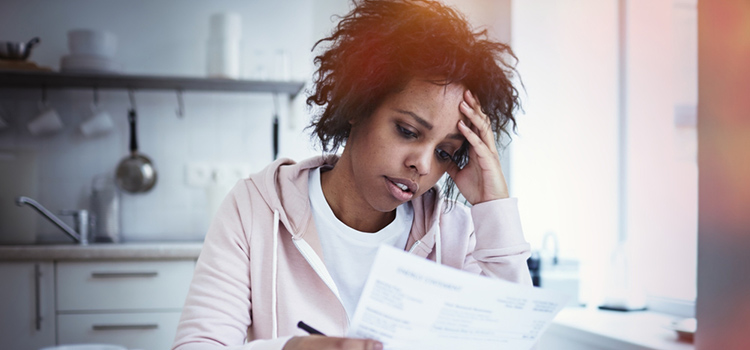

Three Keys to Reducing Financial Stress

When you’re dealing with financial stress, it can keep you from being able to live your life and be happy. Your thoughts of money and bills take over and are always in the front of your mind, which can lead to depression and anxiety. And when that happens, you start to feel stuck, like you’ll never break out of your rut, so you close yourself off to opportunities that could help.

Finances are a source of stress for many people, but they don’t have to be. When you can find ways to reduce your financial stress, you’ll find yourself better able to think of solutions and opportunities will begin to present themselves.

Here are three core strategies for reducing financial stress when things are especially difficult:

Create a Plan

One of the reasons you may feel stress is because you don’t feel in control of your finances. Instead, you feel your finances are controlling you. You feel the constraints of not being able to spend freely and worry about how you’ll pay each bill.

Put yourself back in control by creating a plan. Start by creating a budget. Make a list of all the expenses that have to be paid each month, as well as a list of things that are optional, like gym memberships and movie rentals. Next figure out your actual, take-home income. When you look at the two numbers side-by-side, do you need more money each month or are there a few dollars left over?

Next look for ways to cut expenses by reducing things you don’t need. Then, create a plan for bringing in more income. What kind of side jobs can you find that will bring in a few extra dollars each month? A quick Google search can provide a wealth of ideas.

Create Limits

If you feel like you can’t spend anything, it will only create more stress. Instead, create a spending limit for each of your budget categories. You can buy whatever you need or want, as long as it’s within your spending limit for the month. Make a game out of figuring out where you can save and getting the best price you can find.

If you’re feeling the urge to spend and buy yourself something to cheer you up, that’s okay. Just give it a limit. No more than $5 or $10. Then challenge yourself to find something that will make you happy within that limit.

Get Support

When it comes to money, one thing’s for sure, everyone deals with financial stress at some point. You are never alone in your struggle. Talk to friends and family, let them know what you’re dealing with. When you do, two things will happen. They’ll be more understanding when you tell them you can’t do something and they’ll probably even make more budget-friendly suggestions for spending time together. And, they may have some advice from a time when they dealt with the same issues and overcame them. They may even surprise you by explaining that they’re in the same boat as you, but were to afraid to say anything.

Start a support group with friends and family to share ideas for saving money, budgeting, and reducing your spending on things like groceries and utility bills. Everyone has different ideas, you’ll find great information from others.

Whatever you do, take control of your financial situation and face it head on. It’s the best way to reduce your stress and know that it won’t always be this way.

Article written by Emilie Burke. Emilie writes about overcoming debt, while balancing trying to eat healthy, stay fit, and have a little fun along the way. You can find more of her work at BurkeDoes.com.

No one enjoys feeling stressed about making ends meet. Take control of your finances with these tips to make managing your cash flow a little easier. You can get a free consumer credit counseling session, budget analysis and money management advice with the Union Plus Credit Counseling Program.

Retired IAM Member Stands by the Union Plus Credit Card

Sherman worked on rental trucks for his entire 30-year career. He performed bumper to bumper services on a constantly evolving fleet of trucks.

“I loved being a mechanic and getting a shot at working on all different types of stuff each day – anything that would keep those trucks rolling down the road,” he said. “I also enjoyed the camaraderie with my fellow union members and teaching new mechanics as they came up through the ranks.”

During and after his career, Sherman has used the Union Plus Credit Card for nearly all of his purchases. He appreciates that it is unquestionably a union-backed card.

“I would highly recommend the Union Plus Credit Card to all union members,” said Sherman. “I’ve lived a lot of life and gone through a lot. The folks behind the Union Plus Credit Card have always stuck with me.”

The Union Plus Credit Card is made available in partnership with Capital One. It is backed by the highly rated Capital One Mobile app, which is designed for a simple mobile experience, making it even easier to manage your account. Additionally, eligible card holders may gain access to hardship assistance grants in the event they are in need of specific help through a range of life events.2

To learn more and apply, visit theunioncard.com.

1The Union Plus Credit Card is issued by Capital One, N.A. pursuant to a license by Mastercard International Incorporated.

2Certain restrictions, limitations and qualifications apply to these grants. Additional information and eligibility criteria can be obtained at unionplus.org/assistance.

“I still remember the day 25 years ago when I got the newsletter and saw that there was an offer through my union for the Union Plus Credit Card Program1,” said Paul Sherman, a retired International Association of Machinists (IAM) member.

CWA Member Uses Union Plus DMP Grant to Create New Hashtag: #debtfree

“We had quite a bit of debt,” said Amanda Tanay, a Communications Workers of America (CWA) Local 1075 member. “My husband and I were having a hard time getting rid of it on our own.”

Tanay is copy editor and social media coordinator for Monmouth County, New Jersey’s park system. As she came off an illness that forced her to miss work, her husband lost his job.

“It was overwhelming. We tried to pay minimum balances on our credit cards, and we realized it would take us 20 to 30 years.”

The Union Plus Solution

That’s when Tanay and her husband decided to take control of their situation, and Tanay knew she could access Union Plus Credit Counseling for free through the non-profit organization Money Management International (MMI).

After their free session, the Tanays took the next step, enrolling in a customized debt management plan (DMP). They applied for and received a Union Plus DMP Grant, which defrayed the initial $75 set-up fee for the plan. After one year on the plan, they became eligible for and received $300 to reimburse them for their monthly MMI

“I would definitely encourage any CWA member who is working through challenges with debt to access the Union Plus Credit Counseling benefit, set up a plan and apply for the grant,” said Tanay. “With our plan, we’ll pay our debt off in four years, and the Union Plus Grant on top of it is amazing.”

For more information on debt management, credit counseling and all of the Union Plus Hardship Help benefits, visit unionplus.org/hardship.

Union Plus Consumer Credit Counseling is currently available in the United States, but not available in Puerto Rico, Guam, Virgin Islands, and Canada.

Communications Workers of America (CWA) member Amanda Tanay and her husband were having a hard time getting rid of their debt. Because of her CWA membership, Tanay was able to take control of her situation by utilizing Union Plus Credit Counseling through the non-profit organization Money Management International (MMI).

Should I Repay My Debt or Invest My Money?

The following is presented for informational purposes only.

Do The Math

Just like everything else in your finances, deciding how to best use your money is all in the calculations. Take a look at your debt and calculate exactly how much it will cost you to pay it off. Be sure to include any interest, fees, and penalties into these calculations. It’s important to get a clear picture of your debt so that you can make the best decision for your finances.

Try using the debt calculator over at Credit Karma. It’s a handy way to see how much your debt is costing you, and how much you can save by increasing your payments.

Next, take a look at your after-tax rate of return on any investments you may be considering. Unless you’re investing in a tax-free bond or a tax-sheltered account, you will most likely need to pay taxes on your earnings, which could decrease your actual return, so keep that in mind.

Since the question is whether to repay debt or make an investment, you want to compare two numbers: the difference between the cost of your debt (primarily interest charges) with this hypothetical additional payment and the cost of your debt without any extra payments; and the potential return on your investments.

We want to know if putting this pool of extra money into debt will save us more money than it could earn as an investment. That’s not the whole story, of course, but finding those two numbers will help provide an objective, numerical baseline for your decision.

Examine Your Financial Situation

If you’re carrying a lot of high interest credit card balances, paying off these debts may be the better way to go for now. Paying off those debts will not only save you money (that you can later invest), it can also help improve your credit score. If you’ve been struggling to balance your finances because of debt payments and building strong credit is a priority for you, then debt repayment is definitely the smart option.

If your debt is manageable and your interest rates are low, however, investing some of your funds might be a wise option. Especially if those investments are part of a long-term savings plan and you manage your risk.

Before making the final decision though, it’s wise to make sure you have ample emergency funds set aside. When it comes to investing, the funds you set aside are usually difficult to access, at least for a period of time. And if you have to withdrawal those funds early, it may come with a penalty that could eat into your returns.

Consider Another Option

There’s one other option you can consider and that is finding a middle ground. Use some of your funds to pay down debt, especially the high-interest loans, and some to invest. This way you can achieve both goals at once. Budget for paying down your debt with as much as you can manage each month so that you can get it paid off faster and avoid interest fees. Then start investing by taking advantage of your employer’s savings plan, like a 401(k), where your employer matches some or all of your deposits. This way you can deposit twice as much into your investment account while still paying off those heavy debts and increasing your credit score.

When it comes to making a decision to repay debt or invest, look at all options, do the calculations, then make the decision that works best for your financial future.

If you need more help understanding how to tackle your personal debt, consider speaking with a certified credit counselor. Counseling is free and includes an objective review of your finances, along with suggested resources and next steps to help you reach your goals.

Union Plus Credit Counseling

Union members can get a no-obligation money and credit assessment from certified, experienced consumer credit counselors though Union Plus Credit Counseling. Powered by the non-profit Money Management International (MMI), your free session will cover a complete financial review, assistance in budgeting, advice for working with creditors, and more.

Which is better, paying off debt or investing your money? There’s no quick and easy answer to this question. The decision involves some comparison between what your debt is costing you and what you expect to make in return for your investments. It also involves taking a close look at your financial situation.

When deciding between debt repayment and investing, here’s what you need to consider:

How to Set Up a Debt Repayment Plan with the IRS

But don’t worry, there’s good news. Just like making monthly payments on your credit card, you can make payments to the IRS to take care of your tax debt before they take more aggressive action.

There are a few things to keep in mind when it comes to paying the IRS.

Continue to File

Even if you can’t pay what you owe, you still need to file your taxes. Not filing can add more penalty fees on top of what you’ll be charged for paying late. Not filing your tax return on time can add an extra 5 percent to your unpaid balance every month up to a maximum 25 percent penalty. If what you owe is significant, this penalty can make it much more difficult to repay.

Don't Take Drastic Measures

Owing money to the IRS doesn’t mean you have to file bankruptcy to deal with it. Especially if what you owe it less than $10,000. Many people feel like the IRS will take aggressive action immediately and they have no other choice. That’s not the case. The IRS will first ask you to pay and offer you a few opportunities to do so. Avoiding those requests will leave them no other alternative than to go after your funds so don’t ignore them. Instead, try to work with them.

Consider a Loan

Taking out a personal loan with a low interest rate to pay off your tax bill in full may be a better option than setting up a repayment plan with the IRS. Their penalties and interest rates will be much higher and cost you more money in the long run. Plus, a loan company won’t have the ability to be as aggressive when seeking repayment.

Pay With a Credit Card

If possible, pay your bill, or at least a large amount of it, with a credit card with favorable terms. Even if you can’t pay the whole bill on your credit card, reducing what you owe will make it easier to work with the IRS. Just make sure you have a plan in place to manage the credit card portion of the debt.

Request an Installment Plan

If all else fails, you can set up an installment plan directly with the IRS. Applying for a payment plan is easy to do through the IRS website.

You have three options: short-term repayment (repay within 120 days), long-term repayment with direct debit payments (repay within 72 months), or long-term payment without direct debit payments.

Short-term repayment is for debts (penalties and interest included) of no more than $100,000 and costs nothing to set-up. Long-term repayment plans are capped at $50,000 and come with a set-up fee: $31 if you agree to monthly direct debit payments and $149 ($43 for low income participants) if you pay by another method.

Keep in mind that interest fees, just as with your credit card or a personal loan, will continue to be applied so most of your payment will go toward interest in the beginning.

Make a Compromise

If you owe back taxes and have continued to file your taxes every year, you may qualify for an Offer in Compromise. This will allow you to work with the IRS to reduce the total amount you owe and pay it off in one payment. The IRS will analyze your ability to pay based on your current employment, income, and debt. They will then work with you to settle your debt for an amount they feel is fair based on your financial circumstances.

If you’re concerned about your ability to pay any amount to the IRS, consider speaking with a certified credit counselor first. Credit counseling is free and is a helpful tool for anyone struggling to balance their income with their expenses and debts. It’s also nonprofit and unbiased, so you can feel confident that the advice you are given is in your best interests.

Union Plus Credit Counseling

Union members can get a no-obligation money and credit assessment from certified, experienced consumer credit counselors though Union Plus Credit Counseling. Powered by the non-profit Money Management International (MMI), your free session will cover a complete financial review, assistance in budgeting, advice for working with creditors, and more.

Owing money to the IRS can leave you feeling stressed and buried in debt. Having credit card debt is one thing, but the IRS wants their money and they will take steps to garnish your wages or freeze your bank accounts if they feel you’re not going to pay.

Five Affordable Alternatives to Movie Date Nights

That seems like a lot to spend for just one evening. There has to be a better way to enjoy a date night without breaking the bank. Here are some great ideas for fun dates that you can enjoy in the afternoon or evening without blowing your budget

- Go for a bike ride. A lot of cities offer inexpensive bike rentals you can use to ride around town. Or better yet, take your own bikes downtown. This is a great way to see your city in a new way. You can travel places you can’t get to in a car. Pack a picnic and a blanket in your backpack and enjoy an afternoon outside. Or go for an evening ride to enjoy some star gazing.

- Go to a sporting event. Most major cities have amateur teams. It’s just as fun as a professional game but tickets are a lot cheaper. You can get tickets to a local game for as little as $5. Most stadiums offer snack and beer specials too. Or go to a local high school football game. The game is cheap and so are the snacks at the concession stand, but the game is full of energy and cheering.

- Have dinner with friends. Instead of meeting friends out for dinner at an expensive restaurant, invite them over for a potluck and game night. Invite two or three other couples and have everyone bring a dish to share. After dinner, enjoy a game of Pictionary, Charades, or team Monopoly.

- Go ice skating. Outdoor rinks in the winter are romantic and beautiful, and often inexpensive. You can even go skating in the summer, just find an indoor rink in your area. Many rinks offer special “date night” events with discounted pricing. After skating, curl up at home in front of the fire with some hot chocolate for a good chat.

- Go sightseeing. Most people don’t bother to check out all the sights and attractions their local area has to offer unless they have out-of-town guests to entertain. Decide to be a “visitor” in your city for a day and visit the local attractions. A quick Google search will help you find free and low-cost museums, walking tours, and other attractions to check out. Make a list of the places you want to go and print out information about them so you can be your own tour guide.

Enjoying time together doesn’t have to mean spending lots of money. There are so many options for inexpensive date nights if you just look for them. What will you do this weekend?

Union Plus Credit Counseling

Union members can get a no-obligation money and credit assessment from certified, experienced consumer credit counselors though Union Plus Credit Counseling. Powered by the non-profit Money Management International (MMI), your free session will cover a complete financial review, assistance in budgeting, advice for working with creditors, and more.

Movie date nights are expensive; ticket prices average $12-$15 per person (plus a fee if you purchase online) then there’s the snack bar. Just a soda and popcorn to share will set you back another $15 or more. For two people, a night at the movies, without dinner, will cost an average of $50-$70. If you’re going to dinner beforehand, your night out will be over $100.

Early Warning Signs You're Carrying Too Much Debt

No Savings

If you don’t have an emergency fund, or have very minimal savings, you have nothing to fall back on if you should miss a paycheck or have an unexpected expense. And if you’re living paycheck-to-paycheck, any unexpected expense can put you behind on your bills.

Stress with Unexpected Bills

Does opening the mailbox fill you with dread? Are you wondering what will be there today that you’ll need to pay for? If an unexpected bill causes a strong emotional response, like anger or fear, then your finances are headed for trouble. Having an emergency fund will help to eliminate this dread and give you a little more confidence when you go to the mailbox.

Money is Always on Your Mind

While we all have days of worrying about an upcoming expense, if your thoughts are consumed on a daily basis with worry about your finances or how you will handle your bills, you have a problem.

Hiding Purchases

Most of us are guilty of hiding a purchase from someone because we don’t want them to know we bought a new pair of shoes or something else we really didn’t need, but if this is a habit, something’s wrong. Do you hide your non-essential purchases on a regular basis? If so, it’s probably because you know you didn’t need it and you really can’t afford it so you don’t want anyone to know.

Only Making Minimum Payments

If you’re struggling to make just the minimum payment on your credit card bills or loans, there’s a problem. These types of loans are high interest and will cost you more the longer it takes to pay them off. If you can only manage the minimum payment, it’s time to look at your debt.

Using One Debt to Pay Another

It’s one thing to pay your utility bills with your credit cards to earn points, but if you’re doing it because you don’t have the cash to pay them, that’s a problem. Not only are you going further into debt, you’ll end up paying more with the interest rates on your credit card.

Your Card is Declined

If your credit or debit card is declined when you try to make a small purchase, you’re clearly in trouble. You’re maxing out your credit cards and running your bank account down to its last dollar to get by. This is a big red flag that more financial trouble is coming because it only gets worse from here. Once you’ve drained your accounts and maxed out your cards, how will you pay your bills and buy groceries?

If you can relate to any of these early warning signs that you’re carrying too much debt, it’s time to get a handle on your debt. Consider working with a debt and budget counselor or getting a second job if necessary.

Union Plus Credit Counseling

Union members can get a no-obligation money and credit assessment from certified, experienced consumer credit counselors though Union Plus Credit Counseling. Powered by the non-profit Money Management International (MMI), your free session will cover a complete financial review, assistance in budgeting, advice for working with creditors, and more.

While many people know when their finances are in significant trouble, you may not recognize the early warning signs that you’re carrying too much debt. There are signs you can look out for that will let you know that serious financial trouble is coming and it’s time to do something about it before it gets out of hand. Here are a few warning signs that you may be able to relate to:

Know the Risks Before You Invest in Cryptocurrencies

- Cryptocurrencies aren’t backed by a government or central bank. Unlike most traditional currencies, such as the dollar or yen, the value of a cryptocurrency is not tied to promises by a government or a central bank.

- If you store your cryptocurrency online, you don’t have the same protections as a bank account. Holdings in online “wallets” are not insured by the government like U.S. bank deposits are.

- A cryptocurrency’s value can change constantly and dramatically. An investment that may be worth thousands of dollars on Tuesday could be worth only hundreds on Wednesday. If the value goes down, there’s no guarantee that it will rise again.

- Nothing about cryptocurrencies makes them a foolproof investment. Just like with any investment opportunity, there are no guarantees.

- No one can guarantee you’ll make money off your investment. Anyone who promises you a guaranteed return or profit is likely scamming you. Just because the cryptocurrency is well-known or has celebrities endorsing it doesn’t mean it’s a good investment.

- Not all cryptocurrencies or the companies behind them are the same. Before you decide to invest in a cryptocurrency, look into the claims the company is making. Do an internet search with the name of the company and the cryptocurrency with words like review, scam, or complaint. Look through several pages of search results.

Originally posted by the Federal Trade Commission. All rights reserved.

It’s not just bitcoin. There are now hundreds of cryptocurrencies, which are a type of digital currency, on the market. They’ve been publicized as a fast and inexpensive way to pay online, but many are now also being marketed as investment opportunities. But before you decide to purchase cryptocurrency as an investment, here are a few things to know:

Why Consolidating Debt Can Save You Time and Money

These loans are a good option for people looking to decrease their number of monthly payments, lower their interest rates and achieve a less-stressful financial future. Here are a few commonly asked questions that might help you determine if a debt consolidation loan is the right option for you.

What is the difference between a secured loan and an unsecured loan?

Secured loans, such as a mortgage or car loan, require you to put collateral down to cover the repayment of the loan if you are unable to make your monthly payments. Unlike a secured loan, an unsecured loan doesn’t require collateral, making it a good solution for those looking to consolidate debt quickly and easily.

Should I pick a fixed rate or a variable rate loan?

A variable rate, like most credit cards, is one that is likely to change (increase) over time, causing your monthly payments to also increase. You may receive a lower rate with a variable rate loan, but because it is not guaranteed to remain the same over time, it’s a potentially riskier option.

A fixed rate is one that will remain the same for the term of the loan. With a fixed rate, you won’t have to worry or wonder if your rate might go up – and that means you’ll always know exactly how much your monthly payment is. No surprises.

How long will it take to pay an unsecured loan off?

Unlike credit cards, loans have a pre-determined length of repayment. This means that you know exactly when your loan is paid off and when you’ll be out of debt. You usually have the flexibility of determining the length of repayment based on monthly payment options. Most lenders allow you to choose the due date of your monthly payment so you can prioritize bills to fit your budget.

Are there fees associated with an unsecured debt consolidation loan?

Some lenders charge an origination fee that can range from 3-6% (or more) of the loan amount you consolidate. For example, a $15,000 loan with a 5% origination fee would result in a $750 origination fee, in addition to your loan amount. Loans without origination fees allow you to save on upfront costs.

Unlike many credit cards, most loans do not charge an annual fee. This allows for even more savings when consolidating credit cards into an unsecured loan.

Is an unsecured loan right for me?

A loan can help you consolidate revolving debts so that you can have flexibility in your budget and achieve your financial goals. They are a good option for people who want to find a solution for outstanding debt and stop wasting money on higher-interest credit card balances. When applying, lenders will review your credit history and look for things such as bankruptcy and on-time payment history. Qualification will vary based on the lender you choose.

Does Union Plus have a solution for me?

Yes! If you’re interested in an unsecured loan, click here to learn more or apply for the Union Plus® Personal Loan so you can start saving time and money today!

Do you have several credit cards that you’ve acquired over time, each with its own interest rate, payment due date and balance? Have you ever considered a loan for debt consolidation?

Set Your Financial Goals for the New Year

There are a variety of financial goals you can set that would improve your financial outlook by the end of the year. Here are just a few that can make a big difference:

Create or Increase Your Emergency Fund

Having a well-stocked emergency fund provides peace of mind should an unexpected repair come up and it provides a cushion if you experience job loss or a large medical expense. With an emergency fund, you have an immediate funding source in case of emergency; you don’t need to wait for your next paycheck to get your car fixed or call a plumber. Creating a cushion of cash that you can easily get your hands on if you need it should be a priority.

Reduce or Pay Off Debt

If high interest fees are costing you money, it’s time to get out of debt once and for all. That money can be put to better use. It may take more than a year to get it all paid off, depending on how much you have, but you can make significant progress in a year. Getting out of debt will free up more money for saving and investing, and even allow you to do things you haven’t been able to do before, like start your own business or take a big trip.

Increase Your Income

If you haven’t started creating multiple streams of income yet, this is your year. You don’t need to quit your job, you just need to make more money, and if your boss isn’t giving you a raise, you need to do it for yourself. Creating multiple streams of income allows you to pay off debt faster, increase your savings quicker, have more money to invest and put towards retirement funds. You can start a side business in your free time; the options are unlimited. And, if you do it right, there’s no ceiling on the amount of money you can make, unlike your job. If you don’t have any other financial goals this year, this one should definitely be on your list. It will help you reach all the others.

Live on Less Than You Earn

If you’re over your head in debt, it may be because you’ve been living above your means. It’s time to cut back and start living on less than you earn so you can get out of debt, save money, and live a better life. It’s time to give your budget a thorough exam and look for places to trim. Start with utility bills, entertainment, and grocery spending. If all else fails, it may be time to downsize or trade in your car for a decent used one.

Just because we’re already into 2018 doesn’t mean it’s too late to set financial goals. The sooner you make them, and commit to them, the sooner you’ll reach them. It doesn’t matter if it’s January or July, set your goals and create a plan for reaching them.

Union Plus Credit Counseling

Union members can get a no-obligation money and credit assessment from certified, experienced consumer credit counselors though Union Plus Credit Counseling. Powered by the non-profit Money Management International (MMI), your free session will cover a complete financial review, assistance in budgeting, advice for working with creditors, and more.

While you're making your resolutions for the new year, be sure to include your financial goals as well. There's no time like the present to plan your financial future.